KEY MEASURES FOR INDIVIDUALS

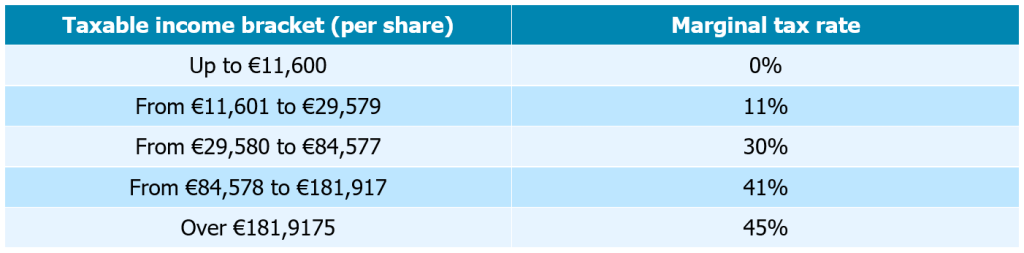

1. Inflation-adjusted income tax scale

The law increases the income tax scale by 0.9% to prevent inflation from artificially pushing taxpayers into higher tax brackets. In practical terms, this reduces the amount of tax payable for many households.

Several tax thresholds relating to income tax are also being adjusted. For example, the deduction limit for maintenance payments made to an adult child is rising to €6,855, whilst the cap on the effects of the family quotient is being raised to €1,807 per half-share.

2. Extension of the tip exemption

The exemption from income tax and social security contributions on tips has been extended until 31 December 2028.

It applies to employees in contact with customers whose remuneration does not exceed 1.6 times the minimum wage, particularly in the hotel, catering and service sectors.

3. Differential levy on high incomes (CDHR)

Originally introduced in 2025, the differential tax on high incomes has been extended.

It is designed to ensure a minimum tax rate of 20% for taxpayers with very high incomes.

It applies in particular to taxpayers whose taxable income exceeds:

- €250,000 for a single person

- €500,000 for a couple

The measure will remain in place as long as the public deficit remains above 3% of GDP.

4. Option for the tax scale and the flat-rate tax

The law relaxes the rules governing the choice between the single flat-rate levy (PFU) and taxation at progressive rates.

From the 2026 tax year onwards, it will be possible to revert to the PFU via an amended return, whereas this option was previously irreversible.

This change offers taxpayers greater flexibility to choose the most advantageous method of taxation according to their circumstances.

5. Increase in the CSG on certain forms of investment income

The Social Security Financing Act for 2026 provides for an increase in the general social contribution (CSG) on certain forms of investment income, from 9.2% to 10.6%.

This increase brings social security contributions from 17.2% to 18.6%, resulting in an increase in the overall rate of the single flat-rate levy (PFU) from 30% to 31.4%.

This applies in particular to dividends, capital gains on securities and certain types of income from assets that are not subject to social security contributions, such as non-professional furnished rentals. However, certain types of income remain excluded from this increase, including property income, capital gains on real estate for private individuals and certain regulated savings products.

6. Crédit d’impôt « services à la personne »

The scope of the tax credit for personal care services has been clarified.

The delivery of meals to the homes of elderly or dependent people is now considered a home-based service.

For services provided outside the home :

- They must be provided by the same organisation or employee as the home-based services

- Their cost must not exceed that of the services provided at home

7. New status for private landlords

The law introduces a new status for private landlords, designed to gradually replace the previous schemes supporting investment in rental property.

The scheme applies in particular to :

- New-build properties or off-plan properties

- Existing properties undergoing major renovation work amounting to at least 30% of the purchase price

Key conditions :

- A minimum rental commitment of 9 years

- Unfurnished rental as a main residence

- Compliance with rent caps and tenant income limits

In return, landlords can amortise part of the property’s purchase cost and deduct this amortisation from their property income, up to a limit of €8,000 to €12,000 per year depending on the type of tenancy.

8. Property tax losses and energy-efficient renovation

The increased ceiling of €21,400 for offsetting property losses arising from energy-efficient renovations of energy-inefficient homes has been extended until 31 December 2027.

9. Retention of the pension allowance

Contrary to the original plans, the 10% tax allowance on pensions has been retained. This means that pensioners continue to benefit from this significant tax relief on their income, thereby protecting their purchasing power.

10. Tax on imported small parcels

To protect local businesses, a tax of €2 per parcel is being introduced on low-value items (worth less than €150) imported from outside the European Union.

11. Doubling of the ceiling for the ‘Coluche’ tax relief

The 2026 Finance Act boosts incentives for charitable giving by doubling the ceiling for the ‘Coluche’ tax relief. The ceiling rises from €1,000 to €2,000 per year, whilst maintaining a tax relief rate of 75%.

Example : a donation of €2,000 will now qualify for up to €1,500 in tax relief.

The measure applies to donations made from the end of 2025, for the 2026 tax return.

This scheme applies to donations made :

- To charities helping people in need (food aid, housing, healthcare),

- To organisations supporting victims of domestic violence.

KEY MEASURES FOR BUSINESSES

1. Revision of the thresholds for the micro-enterprise scheme

The thresholds for the micro-scheme have been revised for the period 2026–2029 :

- Micro-BIC

- Provision of services : €83,600

- Sale of goods : €203,100

- Micro-BNC : €83,600

- Micro-BA : €129,200

2. Tax on asset-holding companies

A new tax on wealth-holding companies is being introduced :

- It applies to the value of certain luxury non-business assets (yachts, classic cars, jewellery, etc.)

- The following are excluded: cash, financial securities and active shareholdings

- A rate of 20% will apply from financial years ending after 31 December 2026

The aim is to increase taxation on high-value assets often used for tax optimisation purposes

3. Special levy on large companies

The law extends the one-off tax on profits for 2026, targeting groups with a turnover exceeding :

- €1.5 billion — rate of 20.60%

- Over €3 billion — rate of 41.20%

This measure aims to ensure that major economic players contribute more towards reducing the deficit.

4. Extended depreciation of goodwill

The option to claim tax depreciation on acquired business assets has been extended for acquisitions made up to 31 December 2029.

This measure is designed to support investment and business succession.

5. Business succession : reform of the Dutreil Pact

The 2026 Finance Act amends the Dutreil Pact, a key scheme offering a 75% exemption from inheritance tax on the transfer or gift of a family business.

Two major changes :

- Exclusion of “non-business” assets (luxury goods, residential property not used for business purposes, works of art, passenger vehicles, jewellery, etc.) from the base eligible for the exemption

- Extension of the individual commitment period for retaining shares, from 4 to 6 years

This reform is primarily aimed at large family businesses. The impact remains limited for the majority of SMEs and micro-enterprises, but nevertheless requires a review of current or future succession plans.

6. Phased abolition of the CVAE

The Corporate Value-Added Contribution (CVAE) will continue to be phased out gradually until 2030. This change reduces the local tax burden on businesses, particularly for SMEs and micro-enterprises.

7. Green Industry Tax Credit (C3IV)

This tax credit has been extended until 2028 to encourage green investment. Certain rules have been amended to ensure compliance with European standards.

REMEMBER

The 2026 Finance Act is based on a balanced approach: controlling public finances on the one hand, and maintaining targeted support on the other.

For individuals, the aim is to protect purchasing power against inflation, whilst increasing the contribution made by high earners and those with significant assets. Measures relating to housing and increases in social benefits are the main levers for support.

For businesses, the approach combines a gradual reduction in certain charges (CVAE), support for strategic and environmental investment, but also a tightening of tax arrangements deemed to be overly optimised, particularly regarding business succession and wealth structuring.

This article was written by the Tax Department of the RUFF & ASSOCIÉS Group in February 2026. Please note that this analysis is current as of today and does not take into account any subsequent changes; the data is subject to change.

Arnaud RUFF

Partner and Chartered Accountant

Charlotte BERBERIAN

Tax Manager